Cuentas wants to turn convenience stores into financial centers

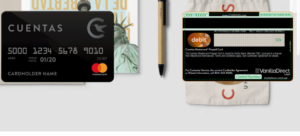

Cuentas, a Miami-based prepaid debit card company targeting Spanish-speaking populations, wants to turn convenience stores into financial hubs through Cuentas-branded debit cards and accounts. The cards, which will launch in early September, will be linked to an online bank account from Sutton Bank. Customers can the reload the cards at any SDI Next convenience store location, of which there are more than 31,000 in major cities across the U.S.

Arik Maimon, CEO of Cuentas, said the company is pitching the additional services that convenience stores offer as a driver for customer acquisition. In addition to Cuentas account top ups, customers can buy and reload public transportation tickets and international calling cards in stores or through the Cuentas app.

The move to turn retail stores into financial hubs is nothing new. For example, Walmart’s Money Services centers offer an array of over-the-counter banking and money transfer services, and 7-11 stores let customers top up their Amazon Cash prepaid cards at checkout.

To sign up for the Cuentas online bank account and prepaid card, customers must have a valid U.S. address. They can then add money to their account at any SDI Next store, as Cuentas acquired a majority stake in SDI Next in 2017. Eventually, the company will offer international remittances through the stores as well, similar to Walmart’s tie-ups with MoneyGram and Ria. Although the app and prepaid cards will be available throughout the U.S., the convenience stores only will be available in New York City, Los Angeles, Connecticut and Michigan to start.

While Cuentas is touting the convenience of the prepaid card offering for the underbanked, the company will charge customers a $3.75 monthly membership fee, a $3.75 one-time activation fee for the card and a $3.95 reloading fee. ATM withdrawals cost $1.50, and balance inquiries cost 75 cents. Getting cash back over-the-counter costs $1.50 as well. By contrast, digital-only banks Chime and Varo offer customers no monthly fees, no foreign transaction fees, a network of tens of thousands of fee-free ATMs and post deposits two days prior to payday.

Still, Cuentas is using other business lines to promote its financial services offerings to its target clientele. The company plans on using its infrastructure as an international calling company to attract its Spanish-speaking customer base to the Cuentas app. Many customers already get texts from Cuentas and TEL3 regarding how much money they have left on their calling plan; Cuentas will begin cross-selling its financial products to these customers via text. The company will advertise through radio and TV commercials as well.

Cuentas, formerly Next Group Holdings, has sold long distance international calling plans for more than 20 years through its subsidiary TEL3, primarily to Spanish-speaking customers. Maimon said the company decided it needed to focus on a new vertical about five years ago, when communication platforms like WhatsApp started making international phone plans a less lucrative business. Next Group Holdings’ first foray into financial services was with its NextCala card and digital bank account, which functioned as a pilot two years ago, he noted, adding that a few thousand people signed up for NextCala at the time.

Maimon said its new prepaid card and bank account will launch sometime within the first two weeks of September, and the company plans to launch international remittance services by the end of the year. Cuentas is working with the Mexico City-based Banco Azteca to launch the remittance service.

Despite the convenience of the SDI Next stores, Cuentas faces a tough challenge gaining customers in a crowded field of prepaid card companies and competitively priced offerings from big-box retailers like Walmart. Meanwhile, challenger banks can incentivize budget-conscious customers by keeping fees low.

Greg McBride, chief financial analyst at Bankrate, said consumers should be wary of prepaid card companies that charge multiple fees. “Even for a consumer that won’t or can’t open a checking account at a bank or credit union, they may find them offering a competitive prepaid card option that avoids the type of ancillary fees that have often characterized the prepaid card space,” he added.

CLOUD