|

| Aite Group, Sept. 2012 |

Arguments across the industry continue over the potential impact and adoption of PFM tools. Despite topping the charts in hype and media coverage over the past several years, some believe that PFM may always fail to deliver in terms of usage rates.

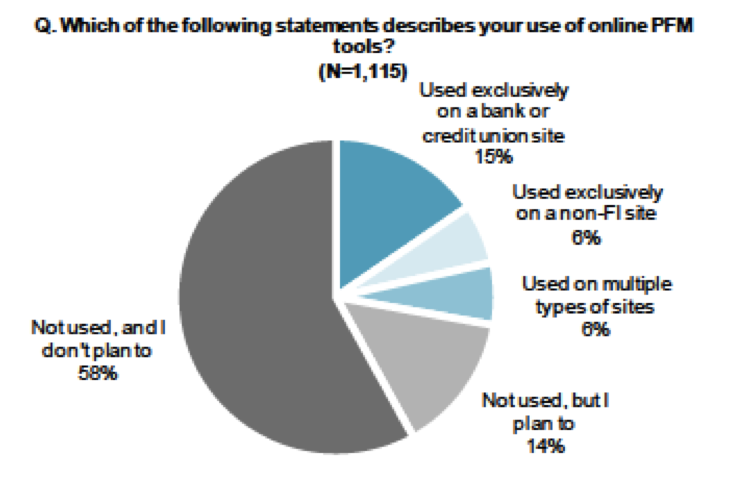

A 2012 survey by the Federal Reserve shows that 21 percent of consumers currently use a PFM tool (this includes any program or website used to track household finances). Aite Group shows that the percentage may be closer to 27 percent when all PFM options are taken into account. However, there is still potential for growth in this area, with an additional 14 percent of consumers indicating a desire to use PFM tools.

|

| Aite Group, Sept. 2012 |

According to Javelin Strategy and Research, nearly two thirds of consumers in the U.S. would like to see all of their financial accounts consolidated in one place (which continues to be a challenge for many PFM applications). Javelin also reports positive consumer feedback to the primary features of a PFM solution as shown below.

Studies also emphasize the value a financial institution can generate by providing a PFM solution that is adopted and utilized by its account holders. These studies show that on average, retention of account holders that use PFM improves by 4% over those that use online banking alone. From a customer acquisition perspective, this can make a huge impact on the financial institution’s bottom line since the industry average for acquiring a new account holder is around $250.00. Assuming an online user base of 100,000 account holders, this equates to $1,000,000 in savings.

So, if the benefits are there from both the consumer and financial institution perspective, why are a relatively few taking advantage of these ‘treats’? Some point to a lack of functionality within the early PFM offerings that have driven the trend since about 2005. Others say that the financial institutions offering PFM as a complement to online banking have not correctly packaged and sold the service. Still others point to the fact that, while people say they want to manage their finances, a significant proportion of those households simply want reports around what they have done as opposed to what they should do (See Ron Shevlin’s Snarketing 2.0 ‘PFM is Dead, Long Live PFM‘).

According to Celent, the barriers are multifold and include technology, experience and behavioral hurdles.

When I attended this year’s BAI Conference in Washington, I was impressed with a firm that is taking a different look at PFM. Provo, Utah-based MoneyDesktopis relying on a unique, eye-catching and dynamic user interface to drive adoption of PFM through consumers’ relationship with their FI. While this may not seem revolutionary, after engaging with the product, I understood how this product could potentially improve the take-up rate at institutions struggling with PFM sign-up and usage.

MoneyDesktop is doing more than just putting lipstick on a pig – its patent-pending BubbleBudgets combines colors, variable sizes and movements to give users an undeniably clear picture of their budget status on a yearly, quarterly, monthly, weekly, or even daily basis.

Use this link to understand the power of this highly visual and engaging solution.

While initially introduced as an online PFM application, MoneyDesktop now includes an even more robust MoneyMobile™ application for smartphones and tablets (demo below). Each application leverages the highly engaging visual elements that made the online application a success. “User experience is absolutely critical no matter what the device,” said Caldwell. “That, paired with the power of our software, is what makes it work. Our mobile and tablet solution have accelerated the path that MoneyDesktop was already on – which was to make sure that peoples’ experience of managing their personal finances was an amazing one.”

As opposed to viewing all of the delivery channels independently, MoneyDesktop introduced it’s Sync Engine at FinovateFall in New York this year. With this tool, data is synched in real-time across all of a user’s devices, and intelligently updated when one device is disconnected from a data signal. The firm also is about to introduce HTML 5 Widgets that will emulate the design available for phones and tablets on a bank’s online banking site. Widgets erase the line that has historically divided PFM from online banking, providing compelling data visualization that is displayed front and center on the Fi’s online banking interface.

Will this combination of enticing form and powerful functionality be enough to move the needle and get customers to embrace a tool they have so far only accepted marginally? Is there a revenue potential to this offering that product developers and marketers can take advantage of? Has MoneyDesktop found the secret formula to success?

The team at MoneyDesktop definitely believes they have found the code to the customer’s heart (and hopefully wallet). They firmly believe that the old style of plugging in numbers and watching bars move up and down is dead. They feel that consumers want to interact with their money and they want to do more than look in their financial rearview mirror.

To date, MoneyDesktop has proven this with FI and consumer adoption rates that trump the industry norm. In the company’s FinovateSpring demo, Caldwell stated that the industry targets PFM adoption rates of 10 to 15 percent, while some MoneyDesktop customers have reached adoption rates as high as 65 percent within a year.

Obviously, the first role as a marketer will be to effectively market the PFM service to customers. I believe the best way to accomplish this is to immerse all employees into the product first so they can provide compelling examples of the benefits of the product to customers. In addition, it is important to provide 1:1 demonstrations of the product since it is difficult to show the benefits of how a customer can manage their finances through even the best video.

Finally, once you have ‘sold’ the PFM solution to your customer, what are your objectives now that you’ve just become the hub for their financial data? With the account holder as the central focus, all of their other checking and savings accounts, credit cards, lines of credit, home loans, etc. are now associated with your institution, even if they are held elsewhere. You have an invaluable 360 degree view of your account holder that opens the door to nearly unlimited cross-sell opportunities, as well as the chance to take their business away from your competitors. That should make any multichannel strategy easier to implement.

Consumers and Mobile Financial Services – Federal Reserve (March, 2012)

How PFM Can Set the Stage for One Stop Online Banking and Define Mobile Banking – Javelin Strategy and Research (Dec. 2011)

Strategies for PFM Success – Aite Group (Sept 2012)

Personal Financial Management 4.0 – Online Banking Report (June 2012)

Personal Financial Management: The Devil is in the Details: Celent (August 2011)

Note:

I am not the only person who has been impressed with what MoneyDesktop offers. MoneyDesktop has left an impression after virtually every show at which it has presented its products, garnering six out of six Best of Show awards in the past year, including FinovateSpring and FinovateFall 2012, CUNA Technology 2011 and 2012, CU Water Cooler Symposium 2012 and BAI Retail Delivery 2012. While awards do not necessarily lead to success in the marketplace, I feel this approach to PFM could help move the needle on both acceptance and usage.