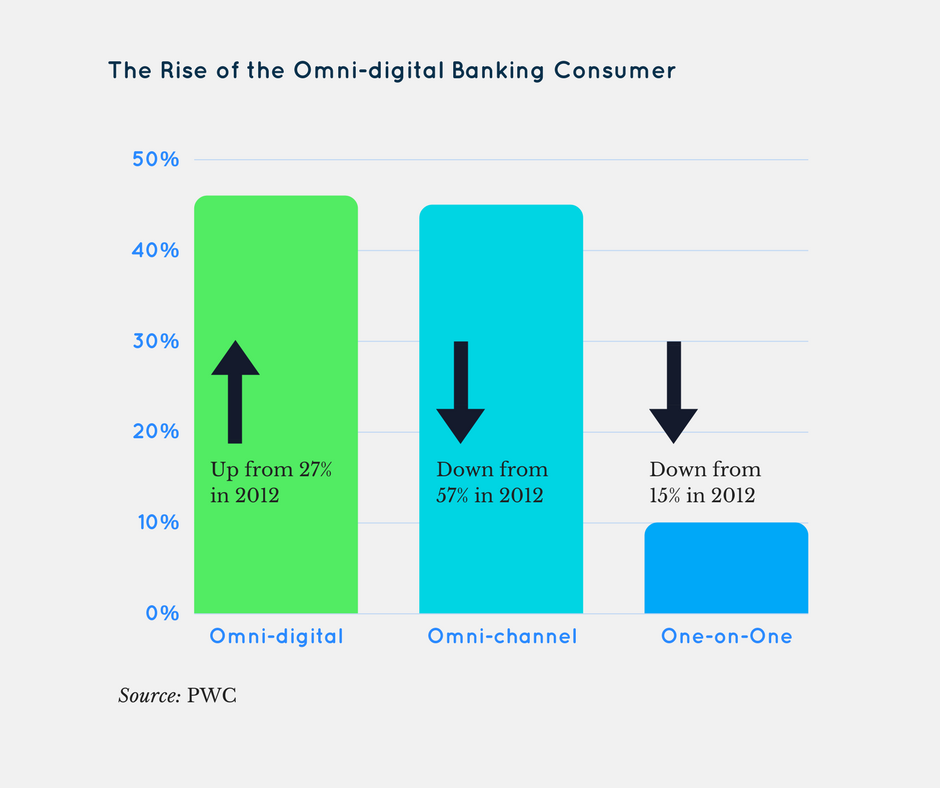

Banks are about to lose SMEs to Amazon

I recently sat down with the marketing team at Anthemis to talk about the changes happening in SME banking and the opportunity for innovation.

Hi John, so why is SME banking getting so much attention at the minute?

Well think of it like this: Traditional banks are built to service three main client cohorts; 1) Large Corporates, 2) High net worth individuals and 3) homogenous retail. They struggle tremendously to service users and customers that sit outside of those parameters. Mass affluent as well as SME customers have become both more distinctive and complex in the last decade and banks haven’t figured out how to service them effectively. It’s becoming something of a battleground.

There have always been small businesses though, what’s changed?

Two main things have changed, 1) there are more small businesses (in absolute terms, not necessarily relative terms) than ever before and 2) many of those businesses have more complex needs than previous generations of businesses. It is no longer reasonable to affix the descriptor SME to all businesses under a certain arbitrary headcount. Traditionally a small business is single jurisdiction, small product base, small customer base, rudimentary financing requirements and low technical sophistication. But new businesses are often multi-jurisdictional from day one, multi-platform and technically sophisticated in everything from equity capital to treasury to accounting and payroll software.

What impact does that have?

It means that the banking experience that these companies require can no longer be serviced by their banks alone and they are looking elsewhere. Examples include crowdfunding for start-up capital instead of traditional collateralised lending products, P2P funding for working capital requirements, new payments services instead of merchant accounts, FX start-ups providing currency solutions and soon a spate of new SaaS based insurance, operations and analytics services via PSD2.

You say it’s a “battleground”, who’s winning?

It may take some time to establish specific winners and losers but it’s clear that new entrants have significant opportunity and upside whilst many incumbents have been more focused on transformation for cost and existing revenue maintenance. There have been very few impactful SME innovations from incumbents over the last number of years, which is shocking given 1) the number of non traditional entrants and 2) the yield opportunity for basic lending products with SMEs. It looks increasingly like the incumbents are going to be blindsided by a rapid shift in SME business landscape between now and 2020. To my mind, it’s the one area, after payments, where banking may well be challenged in the short term.

Can you give more detail on what SME banking might start to look like?

Sure. The first expectation is that ecommerce platforms will act as a launchpad for new propositions. Small and digital only businesses will manage their banking through whatever ecommerce platform they sell through. This will include transaction management, foreign exchange, capital management and tools to manage adjacent necessities like operational efficiency, data acquisition and taxation. The current account equivalent will sit on top of infrastructure provided to the platform through a banking partner. The platform will leverage the data related to the company, including revenue, distribution, product/market trends and conversion figures to generate custom credit scores and capital limits. The “walled garden” in this environment is the customer pool you have access to. If the customer pool is large enough, e.g. Amazon (who stealthily lent over $1bn to SMEs last year), this may be satisfactory. The second expectation is that these platforms will sell data to companies through premium APIs to help generate improved operational efficiency. These services may be provided for free to “customers”.

You also mentioned PSD2, could you elaborate on the likely effect it might have on SMEs?

PSD2 refers to a the second iteration of the European Payments Service Directive. In short, it mandates many things but one notable requirement is that it obliges banks to comply with customer instruction to provide said customers’ payment account data to a licensed third party payment provider through standardised APIs. This will have significant implications for how banks currently do business because it will allow for third parties to piggyback their propositions on infrastructure paid for by banks. Examples will include existing embedded SaaS systems leveraging company cash flow data to provide effectively scored lending products, on demand FX hedges, commoditised insurance propositions and businesses selecting their banking partner based on data the bank can provide to improve operational decisions like product roadmap, premises search or new market entry. Ultimately the relationship a business has with a bank will become increasingly fluid. You won’t have one banking partner, you’ll have many, selecting the appropriate one at the appropriate time for the appropriate task.

So what can banks do to maintain their position?

The process for getting there is straight forward and one we’re proponents of at Anthemis; map your future user needs to clarify the industry model, identify the inferred capabilities chasms and look to partner, venture or invest in order to plug or bridge those gaps. We live in a world where businesses and industries no longer exist in isolation. Industry lines are blurred and successful businesses succeed on their capacity for interoperability. If i can listen to my Spotify in an Uber, I should be able to calculate and pay my VAT in a different jurisdiction through my bank account. There is significant evidence to suggest that banks will have to reenter the SME market through the provision of capital, data and identity infrastructure as a utility rather than a platform. That is not to say that SMEs can’t be a profitable business for traditional banks, but it will necessitate wholesale change in the operating model. If banks don’t solve for those issues particular to SMEs within the next 24 months they will lose to them multi-platform marketplaces capable of deploying money market liquidity into the ecosystem in the form of working capital, start-up capital, asset financing and cheaper invoice financing all the while utilising bank help customer data to do so.

![]()

Banks are about to lose SMEs to Amazon was originally published in #hackingfinance on Medium, where people are continuing the conversation by highlighting and responding to this story.