In Defense of Banks and Bankers

Jamie Dimon

JP Morgan

It’s a hard time to be a banker.

I’ve had this post in my draft folder for a long time, held back from finishing and posting it by the concern that, at least until now, it didn’t seem all that hard to be Jamie Dimon (America’s Banker ™), and he certainly didn’t seem to need a defense. Alas, no longer. The final bastion of respectability and prescience in the banking industry has been resoundingly toppled, and we can now look upon the rout in retrospect and try to glean some lessons.

My conclusion is that the dystopian epic that is the story of late 20th century/early 21st century banking is, at heart, about a group of people asked to do the impossible. For reasons I will articulate below, a catalog of constraints and ill winds conspired to create an unbridgeable gulf between what was asked of them and what they could conceivably achieve with the resources available. Of course, the story is also filled with knaves and opportunists, and probably everyone involved made more money than was reasonable, but in my experience most of the actors were principled, working hard and trying to do the right thing. Jamie Dimon serves us well as an example here. His cardinal sin was not about risk-taking, greed or arrogance, it was his (basically virtuous) ambition to make JP Morgan an important, innovative and growthful company. I believe strongly that those adjectives are not what should be sought by the CEO of a modern bank, and men like Dimon should find other lines of work. All of the industry analysts exhorting our current banking leaders to “Do Better” should be change their tune to simply “Do Less.”

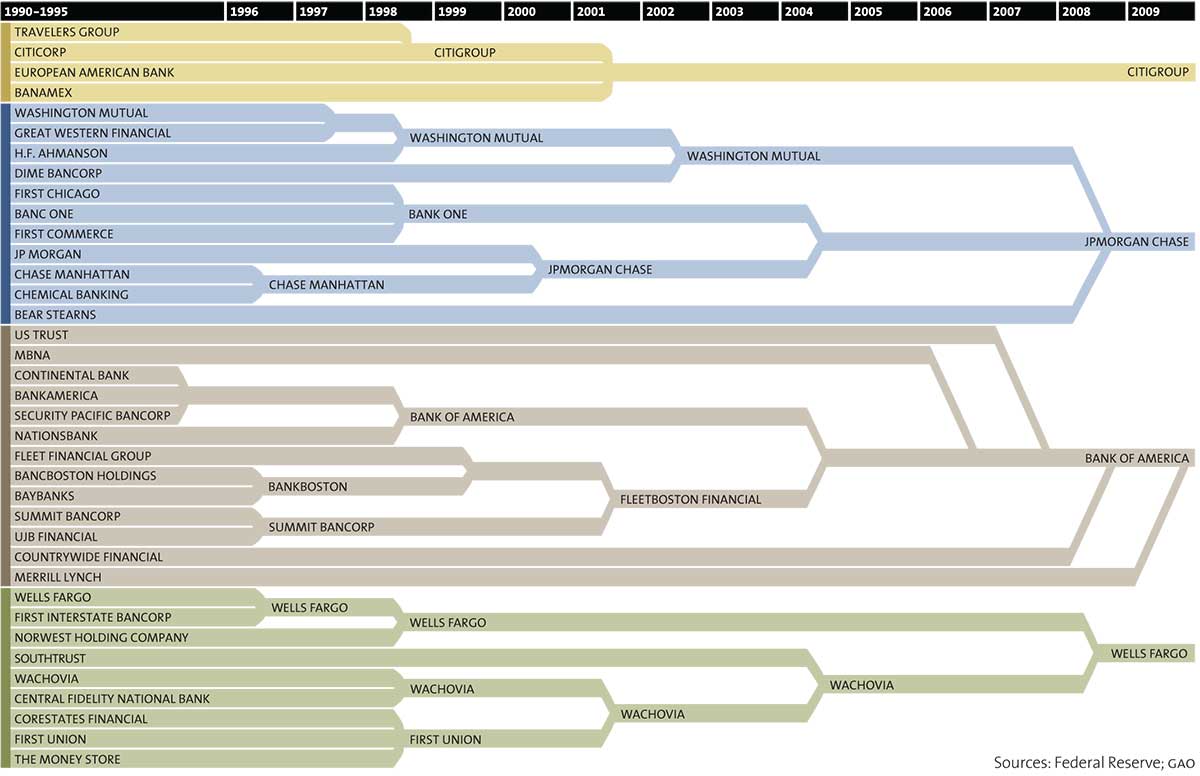

About 10 years ago, I decided to focus my investing career on financial services companies. At the time, this was a bizarre choice for an early stage venture capitalist; I don’t think anyone else in the industry was similarly exclusively focused, and only around 2% of the VC dollars went into the sector. I had a number of reasons for the choice, which I won’t go into in detail, but one of the most significant was my view that the increasingly radical levels of bank consolidation left the industry vulnerable to entrepreneurial competition. As I thought about the industry, there were three key segments: payments, lending and capital markets. In each, the banks had one or several exposed flanks. I wasn’t smart enough to predict the financial crisis, but frankly should have been. It was evident from what I was seeing that the cracks in the dam would turn into deep fissures, in each one of those segments.

It may seem comical to those outside financial services, but there is in fact a robust industry that has grown up around the idea of banking innovation. You could attend a conference every week of the year on the topic, and fill your non-conference hours reading newsletters and blog posts about it. Most of what the pundits think the banks should be innovating around is payments, which is basically the act of moving money from point A to point B. The problem with this idea is that a payment mechanism consists of two things: a technology architecture and a set of rules. The technology part is probably obvious, but the rules part is important and distinctive. Payments is an eco-system business, and the rules define the roles played by all the coordinated but independent parties. By definition, an innovative payment mechanism, one which represents an advance from what exists, involves an exotic and novel technology or a new set of rules — or both. For a variety of reasons, most notably the fact that their systems are a patchwork quilt of archaic, mainframe based architectures cobbled together from the dozens of acquisitions behind each of our large banks, banks are not good at technology innovation [one caveat here: some banks are very good at trading technology, more on that later.] They have to spend nearly all of their time, energy and resources on vital functions like uptime and security, and that leaves very little for the kind of playful tinkering that underlies most breakthroughs.

Banks are even worse at evolving new rules. There are three ways to make new rules, two of which don’t work. The first is to get all parties to agree: FAIL. The second is for a small but powerful cohort to band together and try to exert their will on the others: also FAIL, at least in banking, where despite the consolidation there are still over 8,000 banks in the country, and as many credit unions. The third way is for a renegade establishment to break the existing rules and keep moving fast enough that they get to critical mass before the rule enforcers notice and can do anything about it. Banks are not good at breaking rules, and are really not good at moving fast and avoiding regulators. This is why payment innovation happens by companies like PayPal, Venmo, Dwolla, Zipmark, Simple and Stripe. Is everything they are doing strictly by the book? Not even close. Will some of them achieve escape velocity before they get shut down? Yes. [Am I engaging in the pernicious blogger habit of asking and answering questions? Yes I am. Will I do it again later in this piece? Yes, indeed, I will.]

So in the payments world, banks face critical shortcomings as it relates to innovating. You would think that would be less true when it comes to lending. After all, that is what banks were set up to do in the first place: take in deposits from savers, and turn them into loans for borrowers, making money on the spread in between. To a certain extent, this is still their core mission and they do it well. There are four key dimensions of competition in lending: cost of capital, credit losses, cost of customer acquisition and operating expenses. For a plain vanilla consumer loan, say a mortgage, it’s very hard to beat banks. They pay depositors roughly nothing (very low cost of capital); in ordinary course the FICO or consumer credit score is highly predictive (controlled credit losses); they benefit from large branch networks and high brand recognition (lowering customer acquisition, though online lead gen models have reduced their advantage here); and they run large, systematized factories for processing these loans (low operating costs). But the dirty secret is that there isn’t a lot of money to be made in these commoditized categories, and every once in a while there is a crisis and you lose your shirt. Banks need higher yielding assets, which come in the form of higher interest consumer loans, or business loans of all types.

Not coincidentally, if you canvas the fast growing world of alternative credit now, you will find largely two types of new entrants: high rate consumer lenders (Wonga, Zestcash, Think Finance, Global Analytics, etc) and business lenders (Kabbage, The Receivables Exchange, Capital Access Network, On Deck Capital, etc.) The entrepreneurs are, logically, going where the yield is, and where the banks aren’t (there’s a Jesse James joke to be made there somewhere, but I can’t quite sort it out.) Banks are structurally disadvantaged from entering new areas of lending because the regulators force them to take capital charges against loan types that aren’t tried and true. This negates their cost of capital advantage. By definition, these loan types have short histories in terms of credit performance, and are only vaguely related to existing underwriting strategies, which takes away their credit loss advantage. They probably still have a customer acquisition advantage, but their brands work against them in the consumer categories as they are incredibly skittish about being involved with anything high rate. Finally, while they can be low cost where they have massive scale, at low levels of scale they are horrifically high cost, given average wages and the tendency of highly regulated entities to constantly invent new “i”s to dot and “t”s to cross.

Given the structural disadvantages that face banks when they attempt to innovate in payments and lending, two areas that should be their bread and butter, is it so surprising that they pushed hard to end Glass Steagall and double down on their capital markets businesses? I have this image of a bunch of men in grey (possibly brown) suits, sitting around a board meeting in the mid 1990s, post that credit crisis. One of them stands up in the front of the room and says, “Right, then. We’re facing stiff competition in all of our high margin payments business and we don’t know how to compete. We just got our hats handed to us in mortgage, and all we can do on the lending side is pile the consumer card debt higher and deeper; we’ll do that, but it’ll only go so far. We pushed hard into international, but lost our shirts in Latin America. The way I see it, we can either admit defeat and become the financial equivalents of public utilities, or we can try to be like Goldman Sachs. What’s it going to be boys? ConEd, or the Concorde?” In my mind, the motion to hire the lobbyists was passed unanimously and drinks were served before 5pm.

But there I go, demonizing bankers, which I promised not to do. In fact, my image is flawed. The meetings that caused the problems weren’t backroom meetings like that, they were shareholder meetings, way out in the open. Bank CEOs were being pressured to grow earnings at 10%+/year, when in fact they should be expected to grow as a function of inflation and population. Under that pressure, they behaved like human beings, which is to say they looked for ways to do the impossible. The impossible, as it relates to the third core business of banks, is to prudently grow earnings quickly in a capital markets business.

Let’s look at this most recent JPM debacle as an example of the vise these guys are in. First, you have to realize that these losses ($2-6B, depending on who you ask [my bet would be on or under the low end]) aren’t from one of their trading desks, which are either oriented towards taking positions to make money on them, or taking positions to facilitate a trade for a client. The losses took place in a hedging operation, set up to manage and mitigate risk originating from other parts of the business. There are those who claim that through mission creep, this group ended up making speculative bets way beyond their original brief. I would submit it’s hard to know that one way or another, and that’s just the beginning of the list of things we don’t know. We don’t know what the 1, 3 and 5 year P&L of this group looks like. We don’t know how much profit was generated from the activities that these trades were meant to hedge against. We still don’t know the ultimate disposition of these trades, much less what that would have looked like if JPM hadn’t been forced by the regulators to go public with their positions and forcibly unwind them.

The answers to all of these could be such that reasonable people would look upon these positions, in the context of the track record of the group and the broader business objectives, and say this was bad execution at worst, and a missed putt at the end of a great round at best. What we do know is that even at the high end of the contemplated range, it represents less than a 5% hit to equity, and less than 30% of JPM’s annual profits in any of the last 3 years. Bad news? Surely. Punishable by firing squad? Not in my book. But here’s the best part: Predictable? 100%. What is clear, beyond a shadow of a doubt, is that in capital markets (eerily like in payments or lending), the party that is less regulated is the party who will win. The story of this bad JPM trade is one of the unregulated hedge fund wolves stalking and slaughtering a sheep wearing an electric fence shock collar. Not a fair fight, and expecting that JPM will be a winner in similar fights in the future is laughable.

The good news, for bankers, is that there is a way forward. There is a role, or a set of roles, for banks in all of these business that may not be exciting, high growth or particularly sexy, but can be high margin and massively defensible. Banks should a)manage regulation and compliance; b)manage security/fraud/identity and c)steward depositor capital into risk managed pools. Each of these roles demands a separate blog post, but suffice it to say that each is a critical infrastructure layer across the core segments of banking, and banks are uniquely situated, in terms of current regulation, technology assets, brand identity and culture, to own each layer. By focusing on these roles and not trying to compete with nimbler foes, banks could massively reduce overhead, value at risk and operational complexity. The banks themselves, and the bankers who work there, would go back to being perceived as pillars of the community, literally supporting the entire ecosystem of commerce. Not entirely incidentally (at least not for me), a thousand or more entrepreneurial flowers would bloom, as businesses sprung up around the banks, fulfilling the customer facing and innovation functions that so desperately need to be filled. I predict that companies like American Express (great at payments & brand), Capital One (great at marketing & credit risk) and Goldman Sachs (great at trading technology) would “de-bank”, and choose to partner with Citi, BofA, JPM and others, who would shed many non-core businesses. This restructuring of the financial sector would put the US back on the path to being the global leader in this area, as well as de-risking the global economy.

And as for Jamie Dimon? He should call me. We can do something exciting together. Definitely not a bank.

{kind=link}