Plugging leaks: Bento for Business uses tech to help clients streamline payments

As consumer payments go digital, startups and banks now are focusing on digitizing business-to-business payments, an area where small business owners still are reliant on paper checks and a multitude of expense-management tools.

Bento for Business‘ pitch to business owners, however, is more than just about expense tracking, according to Farhan Ahmad, the Chicago-based company’s CEO. Its series of payment solutions — among them, debit and virtual cards, real-time payments and ACH transfers — seeks to gives business owners more control of “leakage,” or misused funds that often can sink a business. “No matter how much you’re growing at the top of the house, if you have a persistent leak at the bottom of business, you’re going be frustrated,” he said.

For Bento, a five-year-old company, such control is exercised through virtual cards, corporate cards and a Zelle-like ACH payment service called Bento Pay, which it rolled out in July. These activities that can be monitored through the company’s website or app, and its platform also integrates with other digital expense-management platforms. Through these tools, business owners can regulate the limits and types of eligible expenses.

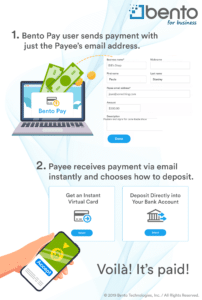

Through Bento Pay, the company is taking Venmo or Zelle-type user experiences (payments to e-mail addresses or phone numbers) and bringing them to the business world. The company is seeing good early interest in Bento Pay, which currently is available to Bento customers and which Ahmad said number in the thousands. Bento customers typically have been 20 and 100 employees, and the company targets non-tech companies that have extensive vendor relationships like transportation companies, grocery shops and non-profits, he noted.

According to Ahmad, business clients using Bento Pay often want to take payments on cards instead of direct deposit ACH transfers and transaction amounts typically run between $1,500 and $2,000, significantly more than most peer-to-peer payments vehicles allow. Bank of America, for example, allows businesses to make Zelle payments, but daily transaction amounts are capped at $5,000. “For some people who are heavy users, we’ve actually seen them immediately use it for all their [payment] purposes,” he said. “We’ve had one or two grocery stores paying all of their suppliers through it.”

Bento for Business isn’t the only company focusing on business-to-business payments or virtual cards (Extend and Brex, for example, offer corporate cards), but what sets Bento apart, according to Ahmad, is the compliance toolkit that it has built in-house. “We have built our own compliance stack, so we can approve and onboard customers instantly in real time,” he added. To avoid the security risks associated with consumer peer-to-peer payments, the company said it institutes KYC checks and has a dispute resolution process to handle fraudulent payments.

Bento generates revenue from subscription fees that clients pay (rates depend on client size and transaction flow), along with interchange fees. The company, which so far has raised $18.5 million in funding, is growing its product offerings as it scales.

Despite its growth, the company is not interested in becoming a challenger bank and is focused solely on resolving money management pain points for small businesses, according to Ahmad. “Our value proposition is we give you more control, more visibility [of payments and expenses],” he said. “If the need for a business is a massive product line, we’re probably not the right company for them.”

Bank Innovation Build, on Nov. 6-7 in Atlanta, helps attendees understand how to “do” innovation better. It is designed to offer best practices, to guide the innovation professional to better results. Register here and save with early bird rates ending September 27th.