Generating Loans With Behavior Triggers

While loan business overall is down, the ability to quickly respond to a customer’s behavior when they are shopping for a loan can be the difference between expanding a current relationship or potentially losing a customer. By leveraging relatively easily accessible credit bureau insight, you can deliver highly relevant communications through multiple channels to generate a steady stream of qualified and ready-to-borrow households.

As the name implies, a loan behavioral trigger lead is created when a customer or prospect is applying for a new loan or is about to refinance an existing loan. Used extensively by the mortgage industry recently due to the large number of households seeking to refinance, triggers also point to households looking for an equity line of credit, new car or even a credit card.

These loan shopper lists are available on a daily, weekly (1-7 days old) or monthly basis (1-30 days old) and are very time sensitive since the candidate is actively seeking a loan or line of credit. As can be expected, using daily triggers is the most expensive due to both the cost of the list and the cost of daily processing/production, but these lists also produce the best results.

The lists can be customized, allowing a financial institution to select candidates based on filters such as credit score, amount of revolving debt, seasoning, LTV, monthly payment amounts, number of recent inquiries on file or any other criteria desired. Phone numbers can also be appended to the lists for an additional charge. History shows that those households with multiple recent inquiries are better prospects since they are considered ‘active shoppers’.

By helping to solve for the mystery of timing, many multichannel loan trigger programs can result in marketing program performance improvement of 5x, 10x or more compared to traditional loan acquisition programs. The challenge for many banks and credit unions is developing an implementation strategy that can process and deliver communications daily and can follow-up on the leads quickly and effectively.

|

| Loan Behavioral Trigger Process |

If the program is focused on identifying current customers shopping for a new loan, there is the potential to connect with these households using direct mail, email, digital communications, mobile and a phone call. This integrated cross-channel strategy is the most effective since most institutions don’t know which channel(s) their customer is most responsive to. In addition, while a phone call and email are the quickest to implement, the penetration of usable/allowable phone numbers and email addresses is limited.

Some banks reach out multiple times using direct mail and email to ensure they are ‘in the mix’ when the customer makes a final lending institution decision, while many financial institutions are using their online banking ‘offer’ pages and even retargeting strategies to keep their message front and center. Due to the time sensitivity, mobile messaging may also be effective if a financial institution has the capability to connect with a customer through texting. In all cases, landing pages are an important component of the communication strategy.

Loan behavioral triggers can also target prospects within a certain geographic area using close to the same strategy. The primary difference is the difficulty in appending as many phone numbers to the files and the hesitation of most organizations to use email for prospecting. Digital communication can still be integrated, however, using advanced geo-targeting techniques combined with SEO tools. With prospecting, integrating a landing page is paramount to success.

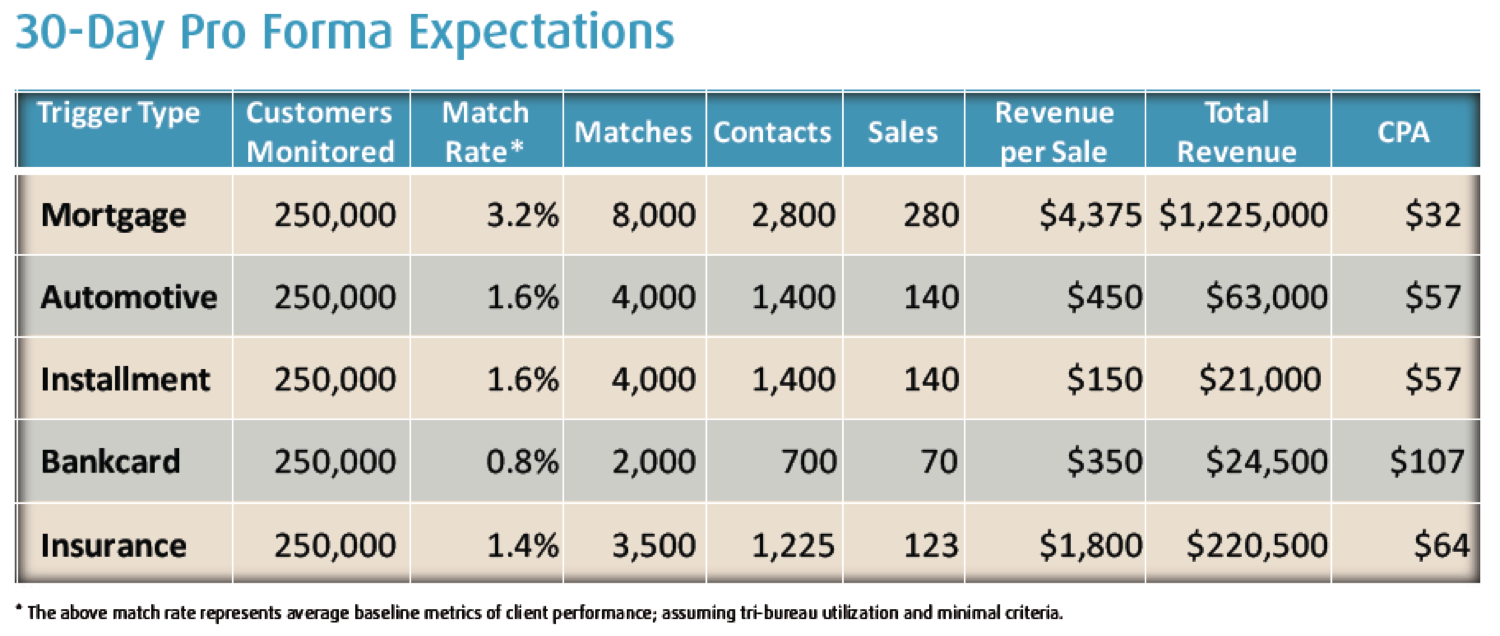

The chart below illustrates the potential effectiveness of a behavioral trigger program built by Datamyx, a provider of tri-bureau data for financial institutions. As can be seen the impact of such a program across product lines can be significant.

List Options

|

| Benefit of Tri-Bureau List Sourcing – Datamyx 2012 |

Creative Messaging

As with any effective direct marketing program, it is important to use creative that clearly states the benefit to the customer as well as how the customer should respond. Since the nature of this marketing communication is in response to a overt customer activity, the communication should be direct with regards to why the customer should include your bank in the competitive set for a new or refinanced loan. If they are a current customer, you should also leverage the power of your relationship with the customer.

All channels should support each other and should provide multiple options for response. A phone number should be provided as well as a landing page where the customer/prospect can initiate the loan application process. Most importantly, since the loan can most likely not be closed online, immediate follow-up by a live representative of the lending area is paramount to the success of the program. Without timely follow-up, the customer/prospect will move to one of the several other alternative organizations that have also reached out to the candidate.

Test and Learn Approach

Behavioral trigger loan marketing requires a ‘test and learn’ approach to determine the most effective list and channel combinations. This is especially necessary given that the most effective trigger based data is derived from a combination of potentially dozens of credit criteria. The payoff for testing alternative strategies is directly correlated to the level of investment in sourcing, creating, evaluating, testing and modifying trigger criteria over time.

Additional Insight: