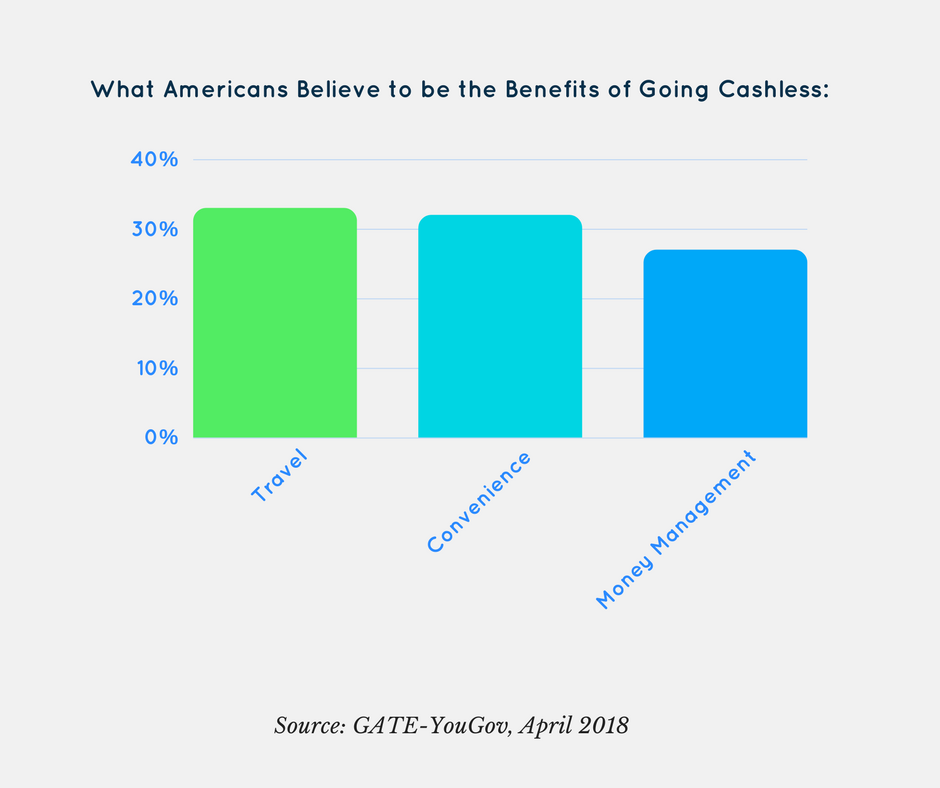

What the Sale of Baidu’s Banking Unit for $1.9B Says About the Future of Payments

Like everything in China, the purchase of Baidu‘s financial services unit by TPG Capital Management LP and Carlyle Group LP today is a big deal.

It is also a deal that will require a big effort by the private equity firms in order to find success. This is a deal that offers a glimpse into the future of fintech — and it’s a tough one to look at.

On the surface, this appears to be a solid acquisition by TPG and Carlyle, two of the world’s largest PE firms. For $1.9 billion — $840 million of which will come from the issues of new shares — the firms get a payments unit with 100 million activated accounts at the end of 2016. No doubt that number is much larger today, just like everything in China.

No doubt, there was a reasonable internal pitch at TPG and Carlyle to do the deal. There’s 1.4 billion people in China … The middle class growth is accelerating in China … Mobile payments is booming in China … Baidu, China’s leading search engine, offers a solid brand and growing userbase from which to continue building the financial services unit, and upon spinoff will be known as Du Xiaoman Financial.

The thing is, Baidu is not Alipay or WeChat Pay, which is owned by Tencent. I am just back from two weeks in China, spending time in Xi’an, Beijing and Shanghai, and the reality is, Alipay and WeChat Pay own — and I mean, own — payments in China. This duopoly has essentially been solidified over the last year or so, at the expense of several other players, including UnionPay, the “old guard” of Chinese payments. Chinese consumers pay for everything with Alipay or WeChat Pay. There’s no room for a third player.

WeChat deserves particular note, especially for innovation teams at Western financial institutions. Generally, financial services in the developed world come from financial institutions. But the social media influence on usage of financial services cannot be overlooked. There has been a taste of this in Venmo, but Venmo remains a standalone application. WeChat is one part Twitter, one part Instagram, one part Whatsapp — and one part Venmo. WeChat possesses a profound convergence of social media functionality into one concentrated application. A financial institution cannot compete with this utility, nor can Baidu.

(What has captured consumers is the QR-driven payments from WeChat and Alipay. The QR code is fast and easy and, from an application standpoint, syncs well with a mobile application’s interface. Mobile is becoming more image-oriented — and the QR is an “image” payments mechanism.)

What can a Western financial institution’s innovation team learn from this? That financial products are not just about the “financial” or the “product” any longer. Financial products — no matter what type — will increasingly need to consider social media dynamics and functionality (hence, the image dynamic), whether for reasons of marketing or utility. In fact, it is possible that WeChat Pay will eclipse Alipay for this very reason.

Sorry, TPG/Carlyle.